Goldman Sachs Identifies Three Key Drivers of China's Economy and Investment Strategies for a Rebound

Original Report Publication Date: March 15, 2026

Executive Summary

Market sentiment surrounding the Chinese economy remains cautious. However, in a recent report, Goldman Sachs examined three key variables influencing China's economic performance and stock market, concluding that there are clear shifts the market may be overlooking.

The core takeaways from this report are:

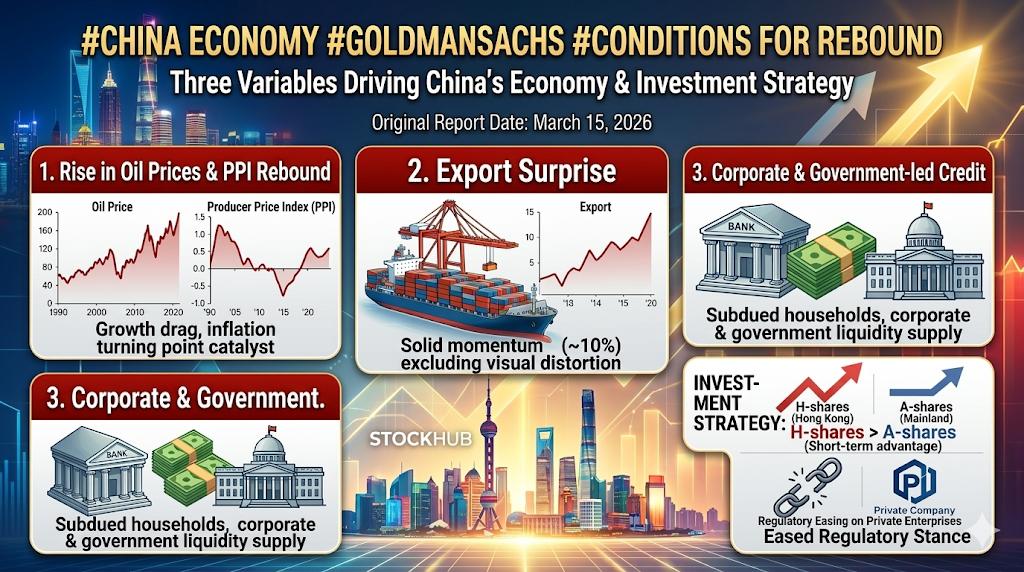

- Rising oil prices due to geopolitical risks, while a burden on China's growth rate, could potentially serve as a turning point for inflation and producer profitability.

- The surge in exports in January-February reflects some calendar effects, but even after removing distortions, the underlying trend remains robust.

- Credit data was stronger than expected, with liquidity supply, particularly from corporations and the government, buffering the economic downturn.

In essence, while the Chinese economy still faces structural challenges, this report's key message is that some core indicators are showing better-than-expected signs of improvement.

1. Impact of Rising Oil Prices: A Burden on Growth, Potential Turning Point for Inflation and Corporate Margins

Goldman Sachs has revised its forecast for the average Brent crude oil price in March-April 2026 upwards to around $100 per barrel, reflecting recent tensions in the Middle East and potential supply disruptions around the Strait of Hormuz.

As China is a net importer of energy, rising oil prices directly burden the macroeconomy. Consequently, Goldman Sachs has slightly lowered its forecast for China's real GDP growth in 2026 from 4.8% to 4.7%.

Conversely, inflation forecasts have been revised upwards:

- 2026 Average CPI Forecast: 0.9%

- 2026 Average PPI Forecast: 0.8%

The most critical point here is the potential for a turnaround in the Producer Price Index (PPI). China's PPI has been in negative territory for over 40 months, pressuring corporate profitability and investor sentiment. However, Goldman Sachs anticipates a high probability of the PPI growth rate turning positive year-on-year in March or April.

This signifies more than just a simple rebound in prices:

- Pressure on companies from declining selling prices may ease.

- Expectations for improved manufacturing profit margins could increase.

- Deflationary concerns may gradually subside.

Ultimately, while rising oil prices are a drag on growth, they could mark the end of a prolonged period of price deflation in the production sector, necessitating a balanced market perspective.

2. The Reality of the Export Surprise: Numbers are Inflated, but Fundamentals Remain Robust

China's nominal exports for January-February 2026 combined increased by 22% year-on-year, significantly exceeding market expectations. While this appears to be a very strong export recovery on the surface, Goldman Sachs points out the risk of taking these figures at face value.

The primary reason is the calendar effect due to the shifting timing of the Lunar New Year. This year, the Lunar New Year schedule differed from previous years, leading to a statistically stronger export figure for January-February.

Goldman Sachs estimates the underlying export growth rate, after removing this distortion, to be around 10%.

While lower than 22%, 10% is by no means a weak figure. Instead, it can be interpreted as an indicator that China's export competitiveness remains intact despite concerns about a global demand slowdown.

However, caution is advised in interpreting future data:

- March exports may appear relatively weak due to base effects.

- An increase in import values due to rising oil prices could reduce the trade surplus.

- Consequently, the current account surplus forecast may also be revised downwards.

Indeed, Goldman Sachs has lowered its forecast for China's current account surplus as a percentage of GDP in 2026 from 4.3% to 3.9%. Nevertheless, this figure remains higher than the market's average expectation.

In summary, for recent export data, one must look beyond the headline numbers to understand the structure. While the headline figures may be inflated, the underlying momentum remains robust, which is crucial.

3. Stronger-Than-Expected Credit Data: Households are Weak, but Corporations and Government are Providing Support

China's credit data for February was better than market expectations. According to Goldman Sachs, both new bank lending and the net increase in total social financing (TSF) exceeded consensus.

Total Social Financing (TSF) is a key indicator showing the total amount of funds supplied by China's financial system to the real economy. This data reveals that the flow of funds within China has not completely frozen.

Specifically, there were clear differences in performance across sectors.

Household Sector: Still Weak

Household lending continued its sluggish trend. This indicates that the downturn in the real estate market and the delayed recovery in consumer sentiment have not yet been resolved. In other words, private consumption and housing-related recovery remain the weak links in China's economy.

Corporate Sector: Gradual Improvement

Conversely, corporate lending has shown improvement in recent months. This suggests that corporations are gradually increasing their demand for funds for investment and operational purposes.

Government Sector: Confirmation of Expanded Fiscal Spending

Goldman Sachs also noted a significant decrease in government fiscal deposits in February. A reduction in funds held in government accounts implies that fiscal spending has been executed in the market.

This is a very important signal:

- It signifies that while households are not yet actively increasing consumption and borrowing,

- Corporate demand for funds and government fiscal execution are supporting the economic floor.

In other words, the current recovery in China's liquidity is not consumption-driven but rather centered around corporations and the government, and in the short term, this structure is buffering the economic downturn.

4. Equity Market Strategy: H-Shares Over A-Shares, and Focus on Policy Receptiveness Shifts

Amidst changes in macroeconomic variables, Goldman Sachs also highlights relative strategies within the Chinese stock market.

Based solely on recent earnings forecast revisions, mainland A-shares have shown relatively better performance than offshore Chinese stocks. However, Goldman Sachs' rotation model suggests that Hong Kong-listed H-shares are likely to achieve modest outperformance relative to A-shares over the next three months.

This is driven by a combination of supply-demand dynamics and changes in the policy environment.

Foreign Investor Positioning: Still Conservative

Foreign investors, including global mutual funds and hedge funds, continue to maintain low allocations to Chinese equities. This implies that there is room for improvement in investor sentiment.

Southbound Flows: Continued Inflows into Hong Kong Market

In contrast, inflows of capital from mainland China into Hong Kong remain strong. Goldman Sachs estimates that Southbound flows have already reached approximately $24 billion year-to-date. This is a significant support factor for H-share supply and demand.

Policy Environment: Easing Stance Towards Private Enterprises

Another notable change is the policy tone. Goldman Sachs assesses, through news-based indicators, that the Chinese government's policy stance towards private enterprises (POEs) has shifted to a "receptive or neutral" territory.

This represents a different environment compared to the past, where strong regulatory risks were the market's primary concern.

Easing Selling Pressure on "National Team" ETFs

Selling pressure from the so-called "national team" ETFs, which were deployed to stabilize the market, has also slowed in recent weeks. This suggests that market supply and demand pressures have eased compared to before.

In conclusion, while A-shares appear robust based on earnings estimates alone, H-shares may offer greater potential for short-term outperformance going forward, according to Goldman Sachs' strategic view.

Final Summary: While Caution is Still Warranted for the Chinese Market, the Direction is Gradually Shifting

In this report, Goldman Sachs emphasizes the need for a more nuanced perspective on the Chinese economy by examining three key variables.

The core points are:

- Rising oil prices, while a burden on growth, increase the potential for PPI rebound and corporate profitability improvement.

- Export figures may contain some distortions, but underlying growth remains robust.

- Credit data was stronger than expected, with continued liquidity supply driven by corporations and the government.

- In the stock market, H-shares may be relatively more attractive over the next three months.

- The policy environment is also shifting towards a more accommodative stance on private enterprises.

In essence, while it is difficult to definitively conclude that the Chinese economy has entered a full recovery phase, there are at least some cracks appearing in the previously overly pessimistic market narrative.

StockHub Insight & Comments

The most important point in this Goldman Sachs report is not an assertion that the Chinese economy has entered a "full recovery" phase, but rather that signs of improvement, which the market has largely ignored, are gradually accumulating.

Particularly noteworthy is the potential for PPI to turn positive. The Chinese market has long suffered from deflationary concerns and pressure on profit margins. A rebound in producer prices could lead to improved corporate margins and investor sentiment. This is not just a simple price rebound but a change that could impact stock market valuations.

While headline export figures might appear overheated, the fact that underlying growth remains close to double digits, even after removing distortions, is a stronger-than-expected outcome. This indicates that China's manufacturing competitiveness has not been entirely eroded.

On the credit front, the weakness of households is a clear drawback, but the fact that government finances and corporate demand for funds are partially compensating for this is significant. This implies that the rebound in China's economy may be driven by policy and corporations rather than consumption.

In terms of investment strategy, the following two points are key:

- Short-term relative strategy: Examine the potential outperformance of H-shares over A-shares.

- Policy beneficiary perspective: Confirm whether the trend of easing regulations on private enterprises continues.

In conclusion, this report is less a message to be aggressively optimistic about the Chinese market and more a signal that the time is approaching to revise the existing one-sided pessimism. Future variables to monitor include the recovery of consumption, the sustainability of the actual PPI rebound, and the continuity of a pro-private enterprise policy stance.

Disclaimer

This material is an informational content reconstructed based on a Goldman Sachs report and is not intended for the purpose of recommending the purchase or sale of specific assets or providing investment advice. Forecasts and interpretations included in the report may change with market environment shifts, and actual results may differ from expectations. All investment decisions and their associated responsibilities lie with the investor.