ANZ & MUFG Economic Analysis Report : Underlying Trend of Falling Inflation and Trump Administration Variables Behind Seemingly Hot Economic Data

[ANZ & MUFG Economic Analysis Report / 26.02.19]

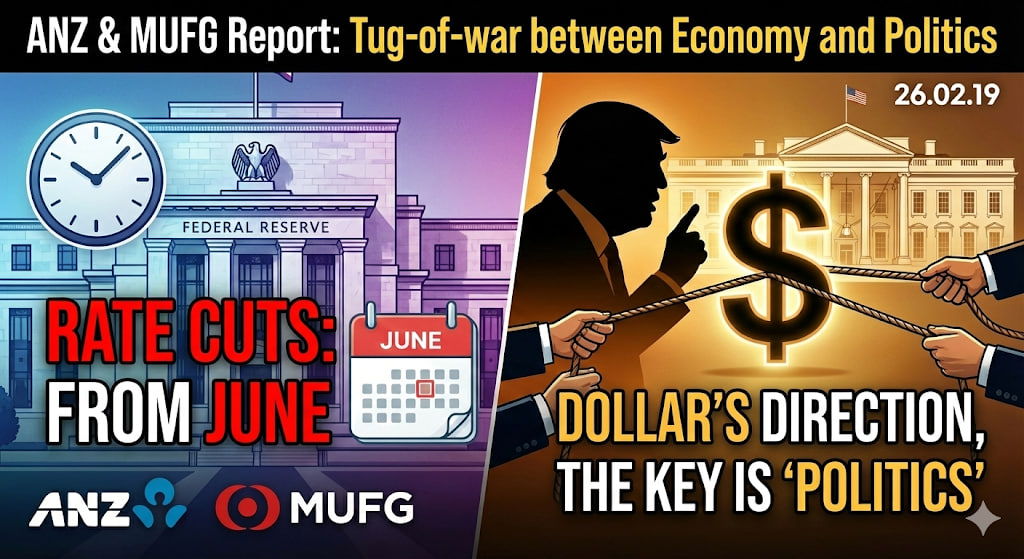

Rate Cuts to Start in June, 'Politics' Key to Dollar's Direction

Subtitle: Underlying Trend of Falling Inflation and Trump Administration Variables Behind Seemingly Hot Economic Data

3-Line Summary

- Delayed Rate Cuts: The Fed's interest rate cuts are expected to begin in the second quarter (around June), not March, with a total of three cuts (75bp) projected for this year.

- Illusion of Indicators: Behind the seemingly robust employment and growth indicators lie real employment decline excluding specific sectors and a trend of falling inflation.

- Dollar Direction and Political Risks: Despite short-term factors boosting the dollar, the Trump administration's policies (tariff reductions, nomination of the next Fed chair, etc.) and concerns about the politicization of the Fed could lead to long-term dollar weakness.

Detailed Analysis

■ 1. Rate Cuts to Start in Q2 (June), Not March

Recent stronger-than-expected U.S. economic data has pushed back expectations for a Fed rate cut. ANZ forecasts that the Fed will hold rates steady in March and resume cuts in the second quarter, around June. Specifically, they expect a total of 75bp in cuts this year, with 25bp cuts in each of the second, third, and fourth quarters. This is because they believe Fed officials can afford to be "patient," waiting for clearer evidence that inflation is slowing further from its current 2.8% level. ANZ emphasizes that, contrary to market concerns, the trend of falling inflation is proceeding rapidly, citing the distinct downward trend in 'Supercore CPI' (4.0% in Jan 2025 -> 2.7% in Jan this year) as evidence.

■ 2. Employment and Economic Growth Creating an Illusion

ANZ diagnoses the recent robust employment and growth indicators as an "illusion."

- Employment Sector: Excluding the 'education and health services' and 'leisure and hospitality' sectors, non-farm payrolls actually decreased by 49,000 in January, a trend that has continued for 11 consecutive months. Wage growth is also slowing, and excess supply in the labor market is increasing, indicating that the real labor market is in a vulnerable state.

- Economic Growth Rate: The average GDP growth rate for Q1-Q3 2025 (2.1%) is below the Congressional Budget Office's (CBO) estimated potential growth rate (2.2%), suggesting the economy is growing within its capacity. They assessed that this level of growth does not trigger inflation, especially due to improvements in labor productivity.

■ 3. Short-Term Factors Supporting a Strong Dollar

Despite the fundamental trend of falling inflation, the reasons for the dollar's immediate strength are as follows:

- Strong Short-Term Economic Indicators: Recent data on durable goods, housing, and industrial production have been stronger than expected, and the January FOMC minutes indicated reduced downside risks to the labor market, leading the market to push back the timing of the first rate cut to July.

- Geopolitical Risks: The surge in international oil prices due to geopolitical risks, such as the possibility of a U.S. attack on Iran, is hitting the euro and yen, which have high energy import dependence, relative to the dollar, boosting the dollar's strength. (In the case of Japan, further downside is expected to be limited due to the unwinding of yen-selling positions after the election of Prime Minister Takaichi and a cautious fiscal policy stance.)

■ 4. The 'Contradiction' of the Trump Administration and the Truth About Tariffs

Both institutions predict that concerns about inflation due to tariffs will be resolved within the year. MUFG analyzed that the Trump administration is likely to implement tariff reduction policies (e.g., India 50% -> 18%, reviewing metal tariff reductions) to control prices ahead of the midterm elections in November this year, which will help bring inflation down to the 2% target. (According to a New York Fed report, "90% of the tariff burden is borne by U.S. companies and households.")

■ 5. The Real Risk: Division and Compromised Independence of the Fed

MUFG identified the 'politicization of the Fed' as the biggest potential risk to the dollar's fundamentals in the future. As Trump nominated Kevin Warsh, who advocates for rate cuts and balance sheet reduction, as the next Fed chair, internal division within the Fed is expected due to policy differences with existing members (who advocate for maintaining high rates to promote economic growth due to AI advancements). If dissenting votes emerge in the policy decision-making process, the market will perceive it as a compromise of the Fed's independence, and such a policy combination has historically been highly likely to lead to dollar weakness.

💡 StockHub Insight & Comments

This report emphasizes the importance of reading the real trends hidden behind short-term economic indicators and headlines that dominate the market. In particular, attention should be paid to the impact of the Trump administration's political calculations (such as tariff reductions aiming for the midterm elections) and the Fed's future moves (concerns about internal division due to the nomination of the next chair) on the dollar's direction.

From an investor's perspective, rather than being reassured by the strong dollar due to short-term favorable indicators, it is time to review portfolios with the fundamental trend of falling inflation, the interest rate cut cycle expected after June, and the possibility of long-term dollar weakness due to political variables in mind.