J.P. Morgan Downgrades Urgently — Oil Shock Engulfs Stock Market

Executive Summary

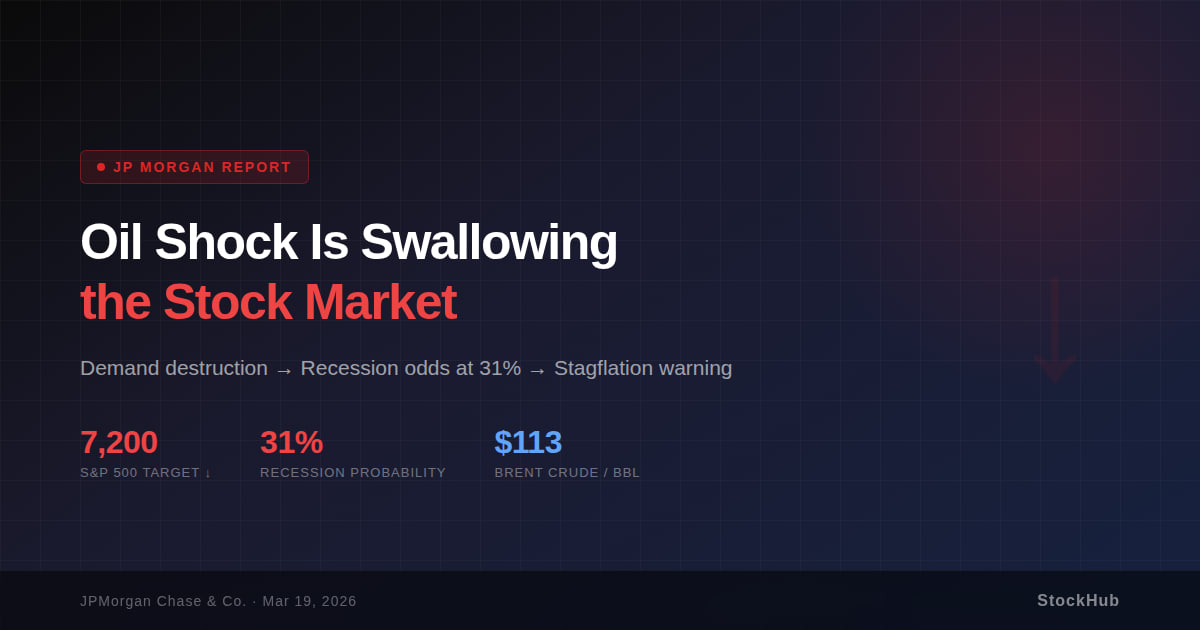

JPMorgan has sharply revised its year-end 2026 S&P 500 target from 7,500 to 7,200. This downgrade signals a warning that the energy shock, triggered by the Middle East conflict, could move beyond mere inflation concerns and lead to demand destruction in the real economy. The probability of a recession has surged from 22% to 31% pre-conflict.

S&P 500 Target Downgrade — Dampening Optimism

JPMorgan equity strategist Dubravko noted that the market is currently pricing in an overly optimistic scenario of "early resolution of the Middle East conflict + early reopening of the Strait of Hormuz."

Typically, stocks and oil prices rise together during economic expansions. However, when an oil price shock of over 30% occurs in a short period, their correlation reverses. The dynamic shifts to oil prices rising while stock markets decline.

The key here is not inflation. The real threat is Demand Destruction. A surge in energy costs simultaneously pressures corporate margins and household consumption, opening a direct path to declining GDP growth and corporate revenues.

JPMorgan warns that if the S&P 500 falls below its 200-day moving average (around 6,600), there will be no meaningful support levels until the 6,000-6,200 range. This explicitly leaves open the possibility of further short-term declines.

Central Bank Dilemma — The Shadow of Stagflation

The surge in oil prices is also disrupting the calculations of monetary policy for various countries.

US Federal Reserve (Fed): Kept the benchmark interest rate unchanged at 3.50-3.75%. Chairman Powell repeatedly emphasized uncertainty, stating it is "still too early" to assess the economic impact and duration of the energy shock. While the median projection for rate cuts in the dot plot remained at one, an increase in the number of members projecting fewer cuts suggests a more conservative shift in internal sentiment.

Europe: The situation is more severe. Expectations for rate cuts are rapidly receding due to the surge in natural gas prices. JPMorgan economists have revised their forecast, expecting the ECB to maintain a hawkish stance without rate cuts this year. They anticipate the Bank of England's (BOE) next rate cut to be pushed back to 2027.

The market has already begun to rapidly price in the combination of rising inflation + slowing growth, i.e., the stagflation narrative. Consequently, JPMorgan suggests tactical positioning with shorts in cyclical stocks (homebuilders, regional banks, transportation) and longs in defense and energy.

China Internet — AI Devouring Existing Platforms

Amidst macroeconomic uncertainty, structural shifts within industries are accelerating. The most dramatic example is the Chinese internet sector.

Tencent Music (TME) plunged 25% in a single day, hitting a 52-week low. The catalyst was not poor earnings, but management's direct admission that "AI-generated content poses a genuine threat to the entire music industry." This is an official acknowledgment that AI's competitiveness has entered a phase of substantially eroding existing platforms' subscription revenues.

Market concerns extend beyond music. The interpretation is spreading that entire existing internet business models, including short-form video, ticketing, and gaming, are at risk of structural disruption due to AI.

Conversely, capital is flowing into new areas. There has been a rapid influx of capital into pure-play AI stocks such as MiniMax and Zhipu. MiniMax's stock price has surged sixfold since its listing, and demand for its core revenue metric, tokens, has exploded sixfold year-to-date. This signals a shift in market valuation criteria from MAU to AI token usage and the success rate of proprietary LLMs.

European Utilities — Opportunities Amidst Government Intervention

In Europe, which has been directly hit by the surge in energy prices, policy interventions to curb electricity prices are expected to be discussed at the EU summit this week.

Investor concerns revolve around scenarios where governments directly claw back profits from power companies. However, JPMorgan analyzes that based on the precedent of the 2022 energy crisis, government intervention only capped the upside of excess profits and did not erode corporate profits themselves. It is highly probable that price stabilization through reforms to the Emissions Trading System (ETS) market will be introduced at the EU level.

Even in an environment of $113 per barrel oil, utility companies' cash-generating capabilities are still assessed as robust. JPMorgan views Centrica (CNA), Drax (DRX), and RWE favorably, citing their low individual country intervention risks.

StockHub Insight & Comments

The core message of this JPMorgan report is clear: "The market has not yet fully priced in the worst-case scenario."

Looking at the current portfolios of institutional investors, including hedge funds, hedging positions against prolonged high oil prices remain insufficient. Volatility is inevitable as the gap between market expectations (early resolution, reopening of the Strait of Hormuz) and reality (escalation, destruction of energy infrastructure) narrows.

From an investor's perspective, three points warrant attention:

First, the market has entered a phase of inverse correlation between oil prices and stock markets. The structure where stock markets decline as oil prices rise may continue for some time.

Second, stagflation positioning. The strategy proposed by JPMorgan, long defense/energy and short cyclical stocks, is rational in the current environment.

Third, capital flow into pure-play Chinese AI stocks. The structural flow of capital from existing big tech to AI-native companies is unlikely to be confined solely to the Chinese market.

This is a time when a strategy focused on risk management and patiently waiting for the next inflection point is more effective than premature bargain hunting.

Disclaimer

This content has been reconfigured and interpreted by StockHub based on a report published by JPMorgan Chase & Co. on March 19, 2026, and is not intended for investment advice or trading recommendations. All investment decisions and their resulting profits and losses are the sole responsibility of the investor. The copyright of the original report belongs to JPMorgan, and the figures and forecasts included in this text are subject to change after the report's publication date.