Goldman Sachs Report: Hormuz Strait Disruption and Energy Supply Chain Crisis

Strait of Hormuz Paralysis and the Energy Supply Chain Crisis — Goldman Sachs Report Analysis

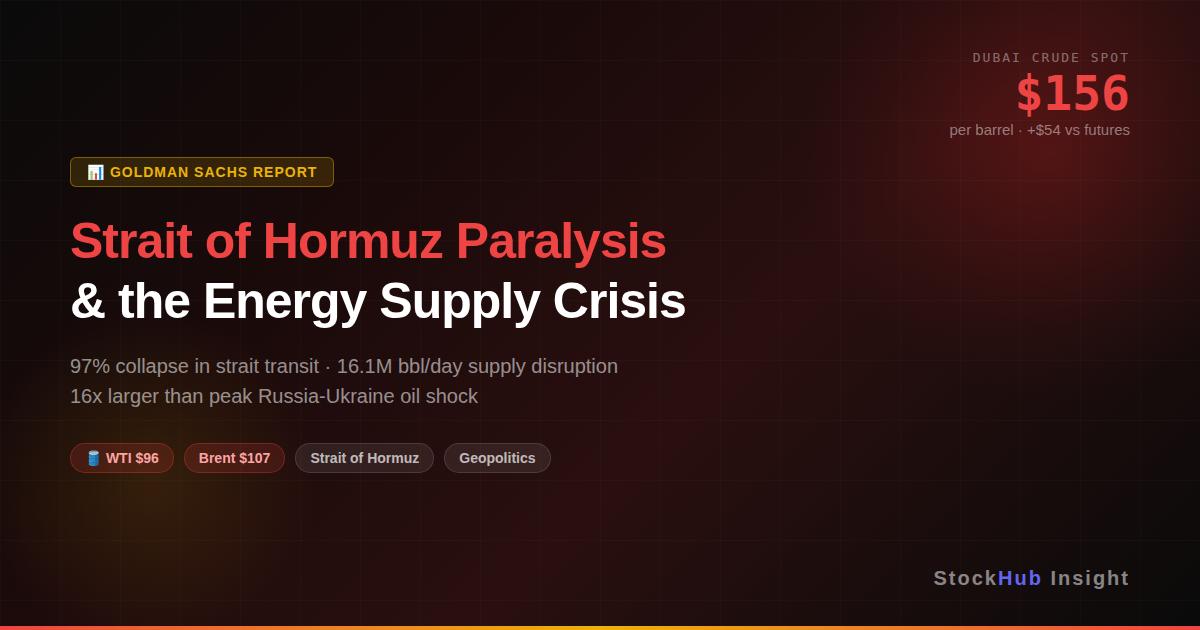

Subtitle: The $156 Dubai Crude Shock, a 97% Shutdown, and a Supply Disruption 16x Larger Than the Russia Crisis

Original report published: March 18, 2026

Key Takeaways

- Strait of Hormuz effectively shut down: Daily oil transit through the strait has plummeted 97% from normal levels to just 600,000 barrels per day. Total supply disruption amounts to 16.1 million barrels per day — 16 times the peak disruption during the 2022 Russia-Ukraine war.

- Extreme physical supply shortage: Dubai crude spot is trading at $156 per barrel, a $54 premium over futures, signaling that refiners are paying extraordinary premiums to secure immediately deliverable crude.

- Brent-WTI spread widening: With Brent at $107 and WTI at $96, the market has begun pricing in the possibility of U.S. crude export restrictions.

Deep Dive

Middle Eastern energy infrastructure is now sustaining direct military strikes, pushing the global crude supply chain beyond psychological anxiety into physical destruction. In its March 18 report, Goldman Sachs concluded that this crisis is not a typical geopolitical risk premium but rather an unprecedented compound supply shock — simultaneous infrastructure destruction and strait blockade.

1. Direct Hits on Energy Infrastructure — How Gas Field Destruction Paralyzes Oil Production

Israeli airstrikes hit Iran's South Pars natural gas field and petrochemical facilities. South Pars, shared with Qatar, is the world's largest gas field. The critical point: Iran relies on natural gas for 79% of its electricity generation. Since oil extraction also requires power, damage to the gas field directly cascades into crude oil production disruptions.

In retaliation, Iran has designated Saudi Arabia's Samref refinery, Qatari, and UAE energy facilities as targets. With both sides now directing strikes at energy infrastructure, the worst-case scenario — physical degradation of the entire Middle East's production capacity — is materializing in real time.

2. Brent $107 vs. WTI $96 — What the Asymmetric Price Response Reveals

Amid the crisis, Brent crude rose 3% to $107, while U.S.-produced WTI stalled around $96. Why would the same commodity move differently?

Goldman Sachs attributes this to the market beginning to price in the possibility of U.S. crude export controls. If the U.S. restricts exports to protect domestic energy security and inflation, global supply tightens (pushing Brent higher), while surplus crude trapped domestically suppresses WTI.

Goldman notes that export controls are not their base case. However, the mere fact that the market is pricing in this possibility underscores the severity of the situation.

3. Dubai Crude at $156 — An Extreme Distress Signal from the Physical Market

The most alarming figure in this report is Dubai crude spot at $156 per barrel — $54 above nearby futures and $53 above Brent futures ($103). This is an extraordinary anomaly.

Normally, spot and nearby futures trade at similar levels. A $54 premium means refiners are effectively saying "we cannot find oil to run our plants" and are willing to pay virtually any price for immediately deliverable crude.

Meanwhile, the Brent spot-futures spread remains within normal ranges. Goldman interprets this as evidence that the extreme supply crunch is still concentrated in the Eastern Hemisphere — where the Middle East is located — and has not yet fully transmitted to Western markets. But whether this firewall can hold if the crisis persists remains an open question.

4. Hormuz Transit Down 97% — Bypass Routes Woefully Insufficient

The root cause of the shortage is the effective paralysis of the Strait of Hormuz, the world's most critical oil chokepoint.

Goldman estimates daily oil flows through the strait have collapsed 97% to just 600,000 barrels (0.6mb/d). Including pipeline diversions, the total volume of crude stranded in the Persian Gulf reaches 16.1 million barrels per day (16.1mb/d). For perspective, this is 16 times the peak Russian oil production disruption during the 2022 war.

Current bypass exports through the ports of Yanbu and Fujairah total around 3.2 million barrels per day (3.2mb/d), but this bypass infrastructure is itself exposed to airstrike risk, meaning volumes could actually decrease. The Iraq-Kurdistan agreement to restart the Kirkuk-Ceyhan pipeline adds only 200,000 barrels per day (0.2mb/d) — a drop in the bucket against the total shortfall.

5. Washington's Emergency Response — Jones Act Waiver and Prolonged Conflict Fears

The U.S. government has moved urgently to contain fuel prices. The Trump administration announced a 60-day waiver of the Jones Act, which normally mandates that cargo shipped between U.S. ports must use American-flagged vessels. This allows foreign ships to transport refined products from the Gulf Coast to the East Coast at lower cost. Goldman estimates this could reduce East Coast refined product prices by $0.60–$0.80 per barrel.

But a quick resolution looks increasingly unlikely. According to prediction market Polymarket, the probability of the Iran conflict ending before March 31 has plunged from 24% last week to just 6%. The Pentagon and Department of Energy have both signaled that resolution will take at least four weeks.

The most concerning scenario: even if the strait reopens, the physical destruction of energy infrastructure could prolong production disruptions for months.

StockHub Insight & Comments

Goldman Sachs' core message is singular and clear: the Hormuz crisis is not a geopolitical risk premium — it is the physical destruction of supply infrastructure.

Three implications demand investor attention.

First, Asian refiners face a cost shock. Dubai crude spot at $156 means crude procurement costs for Korean, Japanese, and Chinese refiners have reached abnormal levels. Near-term earnings hits for domestic refining and petrochemical companies are unavoidable, and the broader Korean equity market faces headwinds given the country's heavy dependence on energy imports.

Second, inflation reignition threatens the rate cut timeline. If oil sustains above $100 for several weeks, the global inflation trajectory resets. The Fed's anticipated second-half rate cuts face further delays, creating a double blow for growth stocks and small caps.

Third, the widening Brent-WTI spread creates positioning opportunities. An asymmetric structure is forming: relative tailwinds for U.S. energy companies, additional burdens for Asian and European consuming nations. This aligns with J.P. Morgan's recommendation in a report published the same week to go long energy and short cyclicals.

This content is a StockHub analysis based on a Goldman Sachs report and does not constitute investment advice or a recommendation to buy or sell any security. All investment decisions are the sole responsibility of the investor.