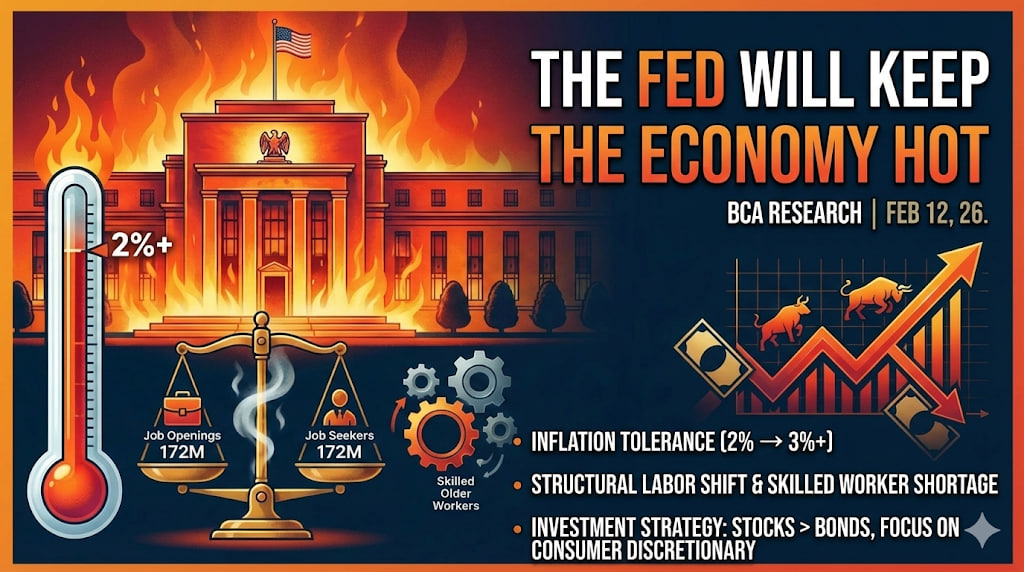

The Fed Will Keep the Economy Running Hot (BCA Research, 2026. 2. 12.)

Why the Fed Might Tolerate an Overheated Economy

Typically, central banks aim to cool down the economy to control inflation. However, BCA Research predicts that the Fed will take the opposite approach this time. The core rationale lies in the structural changes in the labor market since the pandemic.

Currently, the U.S. labor market exhibits a perfect numerical balance, with 172 million job openings and job seekers each. However, the report interprets this not as an ideal state but as a dangerous inflection point. Unlike in the past, when there was either a surplus or shortage of labor, a perfect match means that even a slight decrease in either demand or supply will immediately reduce economic output. Ultimately, the analysis suggests that to sustain growth, the Fed will have no choice but to continue stimulating demand and heating up the economy.

De Facto Upward Adjustment of Inflation Target

This choice inevitably entails higher prices. While the Fed's official target is 2%, BCA diagnoses that the Fed will effectively tolerate inflation between 2.5% and 3.5%.

In fact, the Employment Cost Index (ECI), a wage growth indicator, is currently at 3.4%, exceeding the Fed's ideal target of 3.0%. While some in the market expect AI technology to dramatically increase productivity and curb inflation, the report points out that there are no signs of this in the actual data yet. With wage pressures continuing in the absence of productivity innovation, the Fed is more likely to choose growth over tightening the economy.

Demographic Shifts and the Disappearance of Skilled Labor

The fundamental reason why wage growth is not slowing down despite the supply-demand balance in the labor market is the departure of older workers. According to statistics, approximately 3 million older workers have left the market compared to the pre-pandemic trend.

The problem is that age and experience are not interchangeable in the labor market. Newly entering young workers cannot quickly fill the know-how of older workers with decades of experience. This shortage of skilled labor creates structural wage pressures, which is why the Fed needs to maximize labor participation, even by overheating the economy.

Asset Allocation and Investment Sector Strategy

Under the premise that the Fed will tolerate inflation to promote economic growth, BCA Research suggests the following investment guidance:

Overweight Equities over Bonds: Inflation expectations are likely to rise, leading to higher long-term Treasury yields. This will lead to lower bond prices, making equity assets relatively more advantageous in an environment that tolerates growth over tightening.

Focus on Consumer Discretionary Sector: The consumer discretionary sector has recently underperformed the industrials sector by about 20%, but low real interest rates and a solid labor market will ultimately support consumer purchasing power. Therefore, the current decline is excessive, and a strategy of reducing the weight of industrials and increasing the weight of consumer discretionary is effective.

Reduce Cash and Treasury Holdings: In an environment where inflation remains above the target, cash or long-term Treasuries become less attractive. Portfolio adjustments are needed to prepare for a bear steepening yield curve.

StockHub Comments

The key takeaway from this report is that the Fed's policy priority has completely shifted from price stability to maintaining economic growth. This raises some important considerations for investors.

First, the possibility of an upward revision of the neutral rate. If the Fed tolerates inflation around 3%, the era of low interest rates we knew in the past is unlikely to return for the time being. This is based on the judgment that the economy can withstand even if the benchmark interest rate is maintained at a higher level than before. This will further increase the value of companies with good cash flow that can survive in a high-interest rate environment.

Second, the link between real interest rates and consumption. BCA's reason for recommending consumer discretionary is clear. Even if inflation occurs, if employment is secure and wages keep up, consumers' real purchasing power will not be significantly damaged. In particular, if industrials have risen excessively due to supply chain restructuring issues, finding opportunities in the relatively neglected consumer sector can be a reasonable contrarian strategy.

Third, risk factors. If the Fed intentionally keeps the economy hot and inflation exceeds 3.5% and becomes uncontrollable, the market may be gripped by fear of rapid tightening again. Therefore, even if following the outlook of this report, it is essential to continuously monitor whether inflation indicators deviate from the Fed's tolerance range.

In conclusion, the current market should be concerned not about a recession, but about which assets can defend profits in a high-inflation environment caused by overheating.